It’s now unusual to go a week without a new data breach, but this summer there was a security story with a twist. A million biometric fingerprint scans, mostly unencrypted, were leaked from the unsecured internet database of a South Korean company. The usual advice in similar data breaches is to switch passwords and update software, but how can victims change their fingerprints?

Concerns like these go some way to explain why payment wearables shouldn’t be counted out just yet, despite on the surface seeming less advanced than biometrics.

In fact, there are signs that fintech startups and banks in a number of regions, including Scandinavia, are concentrating their efforts on relatively simple tap-to-pay watches, straps, trackers and jewellery for payments. In August, two of Sweden’s leading banks, Swedbank and Nordea, announced they would start allowing customers with Mastercard debit cards to tap-and-pay for small purchases via wearables, with no new account needed.

Both banks signed up to Fidesmo Pay, a similar system to Apple Pay, to facilitate this and Fidesmo’s chief executive and co-founder Mattias Eld says these schemes are now live, along with a joint-venture in Sweden and Norway with leading partnership bank SEB.

“Additional banks and markets will be launched later this year,” says Mr Eld. “If you want to have a solution based on fingerprints or biometrics, by design you will have a more complex and advanced device or wearable. We fill the space of connecting any device to the banks, some may include fingerprints and some may not.”

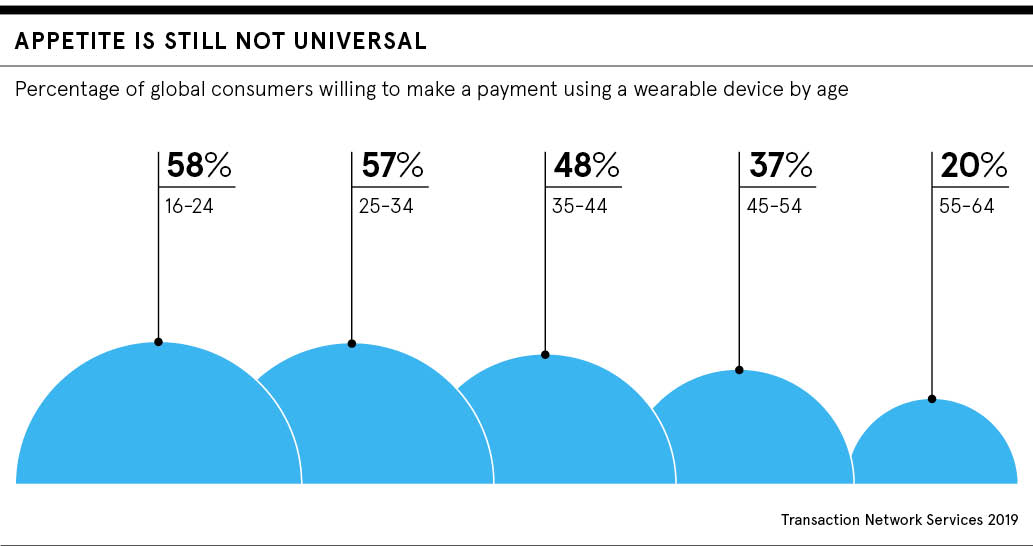

Payment wearables vs smartphone biometrics

Simple near-field communication or NFC-enabled wearables that allow these contactless card-like payments hold a number of advantages over smartphones with biometric sensors and cameras. For one, they’re easy to set up and use with a fairly seamless user experience. As CCS Insight senior analyst, specialising in wearables and virtual reality, Leo Gebbie puts it: “Biometric payments are simply a less developed offering right now.”

Apple has seen success with Apple Pay on the hugely popular Apple Watch series, though with the launch of the Apple Card with Goldman Sachs, it’s clearly exploring all avenues. Elsewhere, Fitbit just added its rival Fitbit Pay to the main model of the new Versa 2 smartwatch, not a special edition as previously.

However, Mr Eld believes it’s “important to offer an ecosystem of services that are independent of the device manufacturer” as this could help open up wearable payments to new kinds of manufacturers which are more fashion oriented.

According to CCS Insight’s data, only 26 per cent of smartwatch owners currently use their wearable device to make payments, but Mr Gebbie expects this to continue to rise “as more smartwatches add features such as NFC” and overall smartwatch shipments grow to 80 million units in 2019.

Beyond Scandinavia, there’s a stark contrast between the UK and China’s approach to biometrics, which may affect trends in payment wearables. “The UK has seen some trials of biometric payment cards, but these have been restricted to small-scale trials, whereas paying with a smartphone or smartwatch is increasingly commonplace,” says Mr Gebbie. “However, in markets such as China, biometric technologies like face recognition are being implemented more widely.”

What are the drawbacks of payment wearables?

Then there’s the security angle. “While biometric payments are designed to increase security around transactions, this doesn’t mean data is entirely immune to being compromised,” says Michael Sawh, editor of wearable tech site Wareable. He points out that with payment wearables, users aren’t required to hand over any sensitive data, but the two methods could also “work in tandem to offer a robust and secure payment setup”.

So, are there any downsides to payment wearables compared with more futuristic face and fingerprint-sensing authentication options? Wearables are an extra cost, for one, and aside from long-lasting devices with swappable batteries, require daily charging. There’s also the possible issue of social etiquette when using smartwatches and wearables to pay; the Apple Watch is a regular sight on the London Underground, but that is not indicative of the UK as a whole.

Arguably, apart from Apple, Fitbit and Samsung, wearables and associated services can be unreliable. Barclaycard merged its bPay and Pingit payment apps earlier this year and Swedish smartwatch Kronaby, which partnered with bPay, filed for bankruptcy in February. “Outside these major players, the wearables space is very unpredictable,” says Mr Gebbie. “It is very difficult for these smaller players to break through and generate meaningful sales.”

With the world’s biggest tech companies seemingly committed to both biometric and NFC-based proximity payments, it seems safe to predict that it’s not an either-or scenario.

It’s now unusual to go a week without a new data breach, but this summer there was a security story with a twist. A million biometric fingerprint scans, mostly unencrypted, were leaked from the unsecured internet database of a South Korean company. The usual advice in similar data breaches is to switch passwords and update software, but how can victims change their fingerprints?

Concerns like these go some way to explain why payment wearables shouldn’t be counted out just yet, despite on the surface seeming less advanced than biometrics.

In fact, there are signs that fintech startups and banks in a number of regions, including Scandinavia, are concentrating their efforts on relatively simple tap-to-pay watches, straps, trackers and jewellery for payments. In August, two of Sweden’s leading banks, Swedbank and Nordea, announced they would start allowing customers with Mastercard debit cards to tap-and-pay for small purchases via wearables, with no new account needed.

Both banks signed up to Fidesmo Pay, a similar system to Apple Pay, to facilitate this and Fidesmo’s chief executive and co-founder Mattias Eld says these schemes are now live, along with a joint-venture in Sweden and Norway with leading partnership bank SEB.